- Energy Tax Facts

- 15 Aug 16

New Report Misses the Mark on Energy Tax Deductions

A new report released by the Council on Foreign Relations analyzes the role of three tax provisions on the oil and natural gas industry in an effort to determine the impact of removing these historic deductions from the U.S. tax code. Unfortunately, the report fails to understand the larger consequences of eliminating these provisions, including the impact on small businesses, the environment, and our nation’s energy security.

Here are five things you need to know:

- Subsidies and deducting standard business expenses are two different things.

First and foremost, it is important to clarify the difference between subsidies and deductible expenses. Subsidies are primarily direct payments from the government for a specific purpose, but they can include some tightly targeted tax reductions, such as certain tax credits. The oil and natural gas industry is not the recipient of these types of payments; however, it is allowed the same business deductions provided to an array of other U.S. businesses.

Deductible expenses, like the Intangible Drilling Cost (IDC) deduction, are costs that companies are able to deduct before they are taxed so companies are better able to recover investment costs and reinvest them into the economy. These provisions are vital deductions, not government handouts, which help thousands of American businesses. Deductions are also available to numerous types of businesses, such as farmers for fertilizer, technology companies for research and development, and even bakeries for supplies and labor. No matter the industry, these are all upfront costs facing nearly every American small business owner with no guaranteed return on investment.

- Report based on price scenarios that do not reflect the current market.

As summarized by the New York Times, the report claims “eliminating the three major federal subsidies for the production of oil and gas would have a very limited impact on the production and consumption of these fossil fuels.” But just how did it come to this conclusion?

This report’s author uses the concept that companies react the same way to price fluctuations as they do to changes in tax reform to determine an “equivalent price impact” (EPI) of repealing existing tax deductions, including IDCs, Percentage Depletion, and the Section 199 manufacturing deduction. To do this, the report uses two price scenarios from the Energy Information Agency (EIA) and International Energy Agency (IEA) for 2030, including EIA’s low oil price scenario of $72/bbl and IEA’s low natural gas price of $3.67/mmbtu – prices well above the current market. Based on these figures it states:

“The EPI from repealing all three tax preferences ranges from -9 to -24 percent. Onshore wells with independent producers represent three-quarters of domestic oil production and face an EPI of -14 percent…These declines in drilling would in turn lead to a long-run decline in domestic oil and gas production. As a result, the global price of oil could rise by 1 percent by 2030 and domestic production could drop 5 percent; global consumption could fall by less than 1 percent.” (emphasis added)

Not only are these substantial impacts to consider, notably offshore where a negative 24 percent EPI is calculated, they also underestimate what the impact would look like in today’s market. While the 2030 scenario prices may provide a glimpse into the future, today’s oil and gas companies are operating in an environment with prices in the $40/bbl and $2.50/mmbtu range, providing a difficult economic market for many companies. An impact of this level would place many operators below a threshold that is economically feasible to operate in, carrying a much heavier impact on domestic production than the report admits.

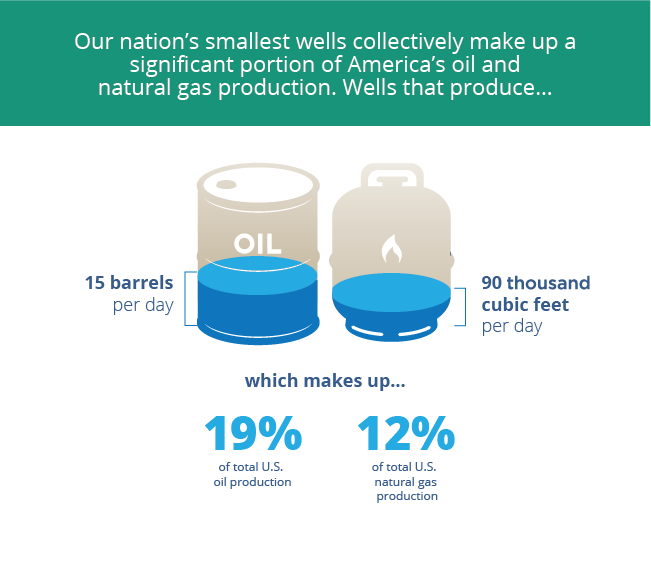

- Small businesses would be the first impacted by removing IDCs and Percentage Depletion

As noted in the report, “The independent producers that have driven increases in U.S. production over the last decade could be hardest hit if low energy prices persist. These firms rely on steady cash flows to continue producing from shale oil and gas fields.” This includes hundreds of small businesses who operate marginal wells across the country, wells that produce under 15 barrels or 90 Mcf a day and make up more than 10 percent of U.S. oil production and of U.S. natural gas production.

Removing deductions such as IDCs and Percentage Depletion, a deduction that enables companies that operate marginal wells to reflect the decreasing value of their resource as it is produced, will have a disproportioned impact on small businesses. It will result in ending production from these wells far sooner than they otherwise would. This logic is exactly why Congress chose to create these deductions in law in the first place.

As accurately described in the report, IDCs also “account for a large majority — between 70 and 85 percent — of the costs of extracting natural resources.” As such, removing the ability to deduct these costs from their taxable income would pose a serious threat to independent producers and their ability to invest in future operations. Given the innovation that has come from previous investments, limiting these companies from exploring new technology and operating areas would stand to the detriment of future energy development.

- Repealing these provisions would hurt the environment.

As noted in the New York Times, the report finds that “in terms of carbon emissions, nothing much would happen at all.” It does, however, find both a negative impact on natural gas production and consumption as well as increased reliance on oil imports – both realities that carry real environmental consequences.

As summarized by the Washington Examiner, the report finds that “Removing the subsidies would have a greater effect on the domestic natural gas industry. Metcalf suggests natural gas prices would rise between 7 and 10 percent and domestic gas production and consumption would fall between 3 and 4 percent.” Given the importance of natural gas in providing affordable, clean-burning energy to millions of American homes and businesses, this projected drop in production should not be taken lightly.

As EIA Administrator Adam Sieminski stated last week, for instance, natural gas is a key reason EIA is projecting 2016 U.S. energy-related carbon dioxide emissions to be at their lowest levels since 1992. As he stated, “The drop in CO2 emissions is largely the result of low natural gas prices, which have contributed to natural gas displacing a large amount of coal used for electricity generation.” The National Bureau of Economic Research also recently released a report on the importance of natural gas in supporting renewable energy development, stating “renewables and fast-reacting fossil technologies appear as highly complementary and that they should be jointly installed to meet the goals of cutting emissions and ensuring a stable supply.”

Increasing reliance on foreign sources of oil also poses an environmental risk. The United States is home to some of the most stringent environmental and safety oversight measures, measures that are not found in many OPEC member countries. As President Obama has stated, “I would rather us, with all the safeguards and standards that we have, be producing our oil and gas rather than importing it, which is bad for our people, but also potentially purchased from places that have much lower environmental standards than we do.”

- Removing these deductions would make the U.S. more reliant on foreign oil, and everything that comes with it.

As the report’s author stated in The Hill, “The fact that oil is a globally traded commodity, how much oil a country imports matters less than the quantity it consumes overall, which is better measure of an economy’s vulnerability to global price volatility.”

While that may be correct from a price standpoint, the reality is that energy imports play a huge role in both our economic and national security. The ability to reduce reliance on foreign sources — ability only achieved through the investments of independent producers — has created a new dynamic for the United States in the global energy market.

In 2015, the White House updated its National Security Strategy to note that the United States is now the “world leader in oil and gas production,” continuing that “American oil production has increased dramatically, impacting global markets. Imports have decreased substantially, reducing the funds we send overseas.” The International Energy Agency has also concluded, “U.S. shale oil will help meet most of the world’s new oil needs in the next five years, even if demand rises from a pick-up in the global economy.”

These are real energy security benefits for the United States, all made possible by increased oil and natural gas development here at home.

Bottom line: America’s oil and gas industry supports jobs, the environment, and our energy security. Historic tax provisions that contribute to the continued successful operations of this industry – the same type of provisions provided to an array of other industries – should not be set aside.

{kind=link}